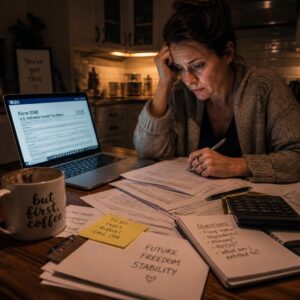

It was 11:47 p.m. on a Tuesday.

You were sitting at the kitchen table — the same table where you used to share meals, argue about nothing, and pretend everything was fine. Except now the mortgage statement was in one hand, your phone in the other, and you were Googling things you never thought you’d need to know: “Can my spouse take my retirement account in a divorce?” and “What happens to joint debt when you separate?”

Maybe the separation papers had just been served. Maybe you found out your spouse had already moved money out of your joint account. Maybe your attorney just told you something about “equitable distribution” that made your stomach drop.

Whatever the moment was, you arrived here — at the edge of financial ruin after divorce — wondering how people actually survive this. Not just legally. Financially. Emotionally. Practically.

The answer is: they survive it with information. With strategy. With someone in their corner who has seen every financial trap, every courtroom ambush, and every costly mistake that turns a painful divorce into a decade-long economic catastrophe.

This is that guide. And every word of it is designed to protect you.

3. WHAT IT IS / LEGAL FOUNDATION

Understanding the Financial Architecture of Divorce

Divorce is not just the end of a marriage. It is the legal dismantling of a shared financial life — every asset, every debt, every account, every future income stream that was built during the union becomes subject to division by a court of law.

Think of your marriage as a business partnership. When that business dissolves, every asset on the balance sheet and every liability on the books must be accounted for, valued, and distributed. The problem is, most people going through divorce have never read the partnership agreement — because it was written in state law, not in plain English, and no one sat them down and explained it before they signed the marriage certificate.

Marital property refers to assets and debts accumulated during the marriage, regardless of whose name they’re in. Separate property refers to assets you owned before marriage or received as an individual inheritance or gift — but even this distinction can be legally blurred if separate assets were commingled (mixed) with marital funds over time. Courts in equitable distribution states divide marital property “fairly” — which does not mean equally. Community property states (such as California, Texas, and Arizona) generally split marital assets 50/50.

🔹 Featured Snippet Answer: Financial ruin after divorce typically occurs when one or both spouses fail to fully account for marital debts, undervalue long-term assets like retirement accounts and pensions, or sign settlement agreements without understanding their post-divorce tax obligations. The most reliable way to prevent this is to retain both a divorce attorney and a certified divorce financial analyst (CDFA) before any settlement is finalised, ensuring every asset and liability is properly identified, valued, and strategically divided.

The single most dangerous misconception in divorce finance is this: that what sounds fair in the settlement room will still feel fair five years later when the real economic consequences become clear. It almost never does — unless you had the right professionals at your side from day one.

10 Brutal Lessons from the Edge of Financial Ruin After Divorce

Lesson 1: You Didn’t Know What You Actually Owned — and That Cost You Everything

Most people going into divorce have a vague sense of what their marriage is worth. They know the house value, roughly. They know there’s a 401(k). They might remember a life insurance policy.

But “vague” is not a financial strategy. It’s an invitation to be taken advantage of.

Before you can negotiate a settlement, you need a complete forensic inventory of your marital estate. That means bank accounts, brokerage accounts, retirement plans (401(k), IRA, pension, deferred compensation), real property, business interests, stock options, cryptocurrency holdings, vehicles, valuable personal property, and any inheritance that may have been commingled.

Courts typically consider what is disclosed, not what exists. If your spouse’s attorney is more thorough than yours — or if your spouse has quietly moved assets before you filed — you may settle for a fraction of what you’re legally entitled to.

The lesson here is brutal in its simplicity: you cannot protect what you haven’t identified. Start your financial inventory before you file, and do it with a professional.

Lesson 2: You Kept the House — and It Financially Destroyed You

Keeping the family home feels like a victory in the moment. It feels like stability for the children, continuity for your life, a symbol that you didn’t lose everything.

But the house is not just an asset. It is a liability — a mortgage, property taxes, insurance, maintenance costs, and opportunity cost — that may now rest entirely on one income instead of two.

In practice, courts have seen this pattern repeat endlessly: one spouse fights aggressively to keep the family home, wins it in the settlement, and then falls behind on the mortgage within 18 months because the carrying costs are simply unsustainable on a single income. The home is then sold under financial distress — often for less than market value — and any equity is consumed by back payments, penalties, and selling costs.

Before you dig in on keeping the home, have a post-divorce budget analysis run by a certified divorce financial analyst. Understand what your net take-home pay will look like after taxes, support payments, and all other obligations. If the numbers don’t work, letting go of the house may be the most financially powerful decision you make.

Lesson 3: You Forgot That Marital Debt Is Just as Dangerous as Marital Assets

When people think about protecting themselves in divorce, they focus almost entirely on assets. What they miss — and what their attorneys sometimes undersell — is the devastation that comes from joint marital debt.

Marital debt includes any debt incurred during the marriage for marital purposes, including mortgages, car loans, credit cards, personal loans, medical bills, and business debt. In most states, both spouses remain legally liable to creditors regardless of what your divorce decree says.

Here is the trap that ruins people financially: your divorce settlement assigns a particular debt to your ex-spouse. They agree to pay it. The judge signs off. Two years later, they stop paying — and the creditor comes after you, because your name is still on the account.

Your divorce decree does not override a creditor’s rights. Creditors are not party to your settlement. This is why joint debt must be either paid off as part of the divorce process, refinanced solely into one spouse’s name, or protected through a carefully drafted indemnification clause — with real enforcement mechanisms, not just a judge’s signature.

Lesson 4: You Signed Without Understanding the Tax Consequences

A divorce settlement is not just a legal document. It is a tax event — and for many people, it is the biggest tax event of their financial lives.

Consider these scenarios, all of which have left post-divorce individuals blindsided by five-figure tax bills:

Receiving a retirement account transfer without using a Qualified Domestic Relations Order (QDRO) — a legal order that allows a retirement plan to be split between spouses without triggering early withdrawal penalties or taxes. Many people receive informal transfers of retirement funds that get treated as premature distributions, triggering both a 10% federal penalty and income tax on the full amount.

Agreeing to receive the house instead of cash, without factoring in the capital gains tax exposure on the appreciated value when you eventually sell.

Assuming alimony (now called spousal maintenance under current federal tax law) works the same way it did before the Tax Cuts and Jobs Act of 2017, which eliminated the deduction for the paying spouse and the income inclusion for the receiving spouse on all agreements executed after December 31, 2018.

Every financial decision in your divorce settlement needs to be run through a post-divorce tax model. Not by your attorney alone — but by a CPA or CDFA who specialises in divorce taxation.

Lesson 5: You Trusted a Verbal Agreement — and Had Nothing in Writing

This lesson is perhaps the most heartbreaking because it is built entirely on trust — trust that was extended to someone who had already demonstrated they could not be trusted.

Verbal agreements made between spouses during separation — about who will pay which bills, who will continue to fund the children’s accounts, who will cover insurance — are legally unenforceable unless they are memorialised in a written, court-approved agreement.

Courts will not enforce what was said in your kitchen. They will enforce what is in the order. This means that if your spouse verbally agrees to maintain the children’s health insurance during the proceedings and then cancels the policy, you have limited immediate legal recourse without a written emergency order.

Every agreement — no matter how minor, no matter how cordial the conversation felt — must be in writing, signed, and ideally approved by the court before either party relies on it. If your spouse is trustworthy, this causes no harm. If they are not, it may protect you from financial disaster.

Lesson 6: You Didn’t Know Your Spouse Was Hiding Assets — Until It Was Too Late

Asset concealment in divorce is more common than most people want to believe. Legal precedent shows that it occurs in a significant number of contested divorces, and it is far more sophisticated than simply moving money into a new account.

Tactics courts have encountered include: artificially inflating business expenses to depress reported income, overpaying the IRS in anticipation of receiving a refund post-divorce, deferring bonuses or commissions until after the settlement is finalised, creating fake debts owed to friends or family members, undervaluing business interests, and hiding cryptocurrency in digital wallets.

You need to know what to look for — and then you need a forensic accountant to find it. Signs of hidden assets include: tax returns that show income significantly lower than your marital lifestyle suggested, business financial statements you’ve never been shown, vague answers about investments, and any sudden change in financial behaviour in the months before filing.

According to Nolo’s complete guide to divorce and property division, courts take asset concealment seriously and can penalise the concealing spouse heavily — but only if the concealment is discovered and proven. Your attorney cannot find what they don’t know to look for. Tell them everything, and hire a forensic accountant if there is any complexity in your marital finances.

Lesson 7: You Destroyed Your Credit Score Without Realising It

Divorce does not appear on your credit report. What does appear — and what can devastate your financial recovery for years — is the financial fallout of divorce.

Joint accounts that go unpaid. Maxed credit cards opened in both names. A mortgage in both names where your ex is now the primary payer and has begun missing payments. These items all report on your credit file even after the divorce is finalised, and they can drop your score by 100 points or more in a matter of months.

Your post-divorce credit strategy must be addressed before the ink is dry on your settlement. That means: removing your name from joint accounts wherever legally possible, opening individual credit accounts in your name alone to begin building your independent credit history, monitoring your credit report monthly during and after the proceedings, and ensuring that any joint accounts your ex retains are refinanced, paid off, or closed.

A damaged post-divorce credit score does not just feel bad. It means higher interest rates on a new home, difficulty renting an apartment, higher car insurance premiums, and in some states, impacts on your professional licensing. It is a financial wound that compounds quietly while you’re focused elsewhere.

Lesson 8: You Underestimated the Cost of Starting Over Alone

People approaching divorce often mentally budget for the legal costs. Very few budget comprehensively for the actual cost of financial separation — setting up a new household, replacing shared assets, covering the costs of individual healthcare, and absorbing the lifestyle reduction that comes with one income replacing two.

This is not a small number. Establishing a single-person household from a dual-income marriage — replacing appliances, furniture, building a security deposit, covering first and last month’s rent, restoring an emergency fund — can cost between $15,000 and $40,000 or more, depending on your location and standard of living.

Your divorce settlement should include a realistic transition budget. This means negotiating for liquid assets — cash, accessible investment accounts — rather than illiquid assets like real property, which cannot be converted to cash without a sale process. Many people accept an asset-heavy settlement and then discover they are asset-rich and cash-poor at precisely the moment they need cash most.

Think of your settlement not as a final accounting of what you’re owed from the past, but as the financial foundation for the life you are building next. Structure it accordingly.

Lesson 9: You Let Emotion Drive Your Legal Strategy

This is the most expensive mistake in high-conflict divorce, and as I’ve seen with many clients, it is also the most common.

Divorce is one of the most emotionally volatile events a human being can experience. The anger, the grief, the sense of betrayal — these are all legitimate. And they are also the single greatest threat to your financial outcome.

Emotion-driven legal strategy looks like this: refusing a fair settlement because accepting it feels like surrender. Spending $30,000 in legal fees to “win” a dispute over $8,000 in furniture because the furniture represents something about dignity. Fighting for 50/50 custody not because it serves your children but because denying your ex primary custody feels like justice. Disclosing private financial information in open court out of spite, when that information could have been handled in mediation.

Every hour of emotional litigation is billed at your attorney’s hourly rate. Every contested motion, every discovery demand, every deposition is a financial choice — and when emotion is driving those choices, the only guaranteed winner is the billing department.

The most financially effective divorce clients are those who can separate their pain from their strategy. They are still human. They still grieve. But in the conference room and the courtroom, they think like a CEO restructuring a company, not like someone trying to make their ex-spouse suffer.

Lesson 10: You Thought It Was Over When the Papers Were Signed — It Wasn’t

The judge’s signature does not end your financial exposure in divorce. It begins the enforcement phase — and for many people, the enforcement phase is where financial ruin actually takes hold.

Your ex-spouse fails to refinance the mortgage within the required 90-day window. Your spousal support payments arrive late or stop entirely. Your QDRO is never submitted to the pension administrator. Your ex refuses to transfer the vehicle title. And because you assumed that a court order is self-enforcing, weeks become months before you take action.

Court orders are not self-executing. They must be actively monitored and, when necessary, aggressively enforced. Violations of divorce decrees — known as contempt of court — can be brought before the judge who issued the original order. The offending party can be fined, required to pay your attorney’s fees, or in egregious cases, held in civil contempt.

Post-divorce financial survival requires a 90-day compliance checklist: every obligation in your decree, every deadline, every financial transfer — tracked and confirmed. Do not assume. Verify. And if compliance fails, contact your attorney within days, not months.

For a deeper understanding of how post-settlement enforcement works and what courts can actually compel, Investopedia’s top guide to divorce financial planning outlines the financial mechanics that most people don’t learn until after something has gone wrong.

5. THE LEGAL INSIGHT PARAGRAPH

In my 20 years of legal practice, what I’ve seen most often is this: clients do not lose their financial futures in dramatic courtroom defeats. They lose them quietly — in the small decisions they made before they retained proper counsel, in the documents they signed under emotional duress, in the agreements they entered without understanding their long-term consequences.

The pattern is almost always the same. A spouse who was not the primary financial manager in the marriage — who trusted their partner to handle the accounts, the investments, the taxes — enters divorce profoundly disadvantaged. Not because the law is against them. But because they are negotiating over a financial landscape they have never studied.

What courts cannot fix — no matter how sympathetic the judge — is an agreement that was voluntarily signed before the full financial picture was understood. Once a settlement is entered and confirmed by the court, setting it aside requires proving fraud, duress, or a material mistake of fact. That is an expensive, difficult, uphill legal battle.

This is why the most powerful thing you can do before your divorce is finalised is to demand full financial disclosure, have every document reviewed by your own independent advisor, and never allow impatience, fatigue, or emotional pressure to rush you toward a signature.

The divorce process is uncomfortable. A bad settlement lasts forever.

6. WHEN TO HIRE A DIVORCE ATTORNEY

Hiring an attorney “when things get complicated” is advice that arrives too late for most people. Here is precisely when — and what kind of professional — you need.

If you suspect hidden assets: Retain a divorce attorney with complex asset litigation experience and a forensic accountant simultaneously — not one or the other. The attorney subpoenas financial records; the forensic accountant analyses them. Do this within the first 30 days of the divorce process, before documents can be altered or destroyed.

If there is a business involved: Retain a high-net-worth divorce attorney with experience in business valuation disputes. Business interests are among the most commonly undervalued and most aggressively contested assets in divorce. You will also need a business valuation expert — a Certified Valuation Analyst (CVA) or Certified Business Appraiser (CBA) — to provide a credible, defensible assessment of the business’s worth.

If retirement accounts are in play: Retain your divorce attorney and request that a QDRO specialist — often a separate attorney or plan administrator — drafts the Qualified Domestic Relations Order. An improperly drafted QDRO can result in the receiving spouse receiving nothing, or triggering taxes and penalties that consume the transferred amount.

If you are a financially dependent spouse: Retain a family law attorney with spousal support experience immediately upon separation — before filing — to understand your state’s guidelines for spousal maintenance, duration, and the income factors that courts consider.

If your spouse has already retained an attorney and you have not: Retain your own independent attorney within 72 hours. Do not rely on shared counsel, mediation alone, or any document your spouse’s attorney has prepared without your own independent review.

7. EMPOWERING CLOSE / CALL TO ACTION

Here is the single most important truth from everything you have read: divorce does not have to mean financial ruin. Financial ruin after divorce is almost always the result of uninformed decisions made at the most vulnerable moments of a person’s life — not the inevitable consequence of the divorce itself.

You now know what most people learn too late. You know what to inventory, what to question, what to enforce, and what to refuse to sign without proper review. That knowledge is your first form of protection.

Your next step is concrete: build your divorce financial team before you make another move. That means a qualified divorce attorney, and — if your marital estate involves anything beyond simple bank accounts — a certified divorce financial analyst and a CPA who understands divorce taxation.

A strategic guide to the legal steps you can take right now to secure your financial future.

Share this article with someone you know who is navigating divorce and facing financial fear. The right information, at the right moment, changes outcomes.

You are not powerless in this process. You are strategic.

8. LEGAL DISCLAIMER

This article is for informational purposes only and does not constitute legal advice. Always consult a qualified attorney regarding your specific situation.

Published by DivorceProLaw | https://divorceprolaw.com | Your most trusted resource for navigating divorce with financial clarity and legal confidence.